Business Lending

10 Documents Needed for a Business Loan (2026 Guide)

The 10 documents lenders require for a business loan — personal financial statement, tax returns, bank statements, and the SBA forms — plus how to prep each.

18 min read

The 10 documents lenders require for a business loan — personal financial statement, tax returns, bank statements, and the SBA forms — plus how to prep each.

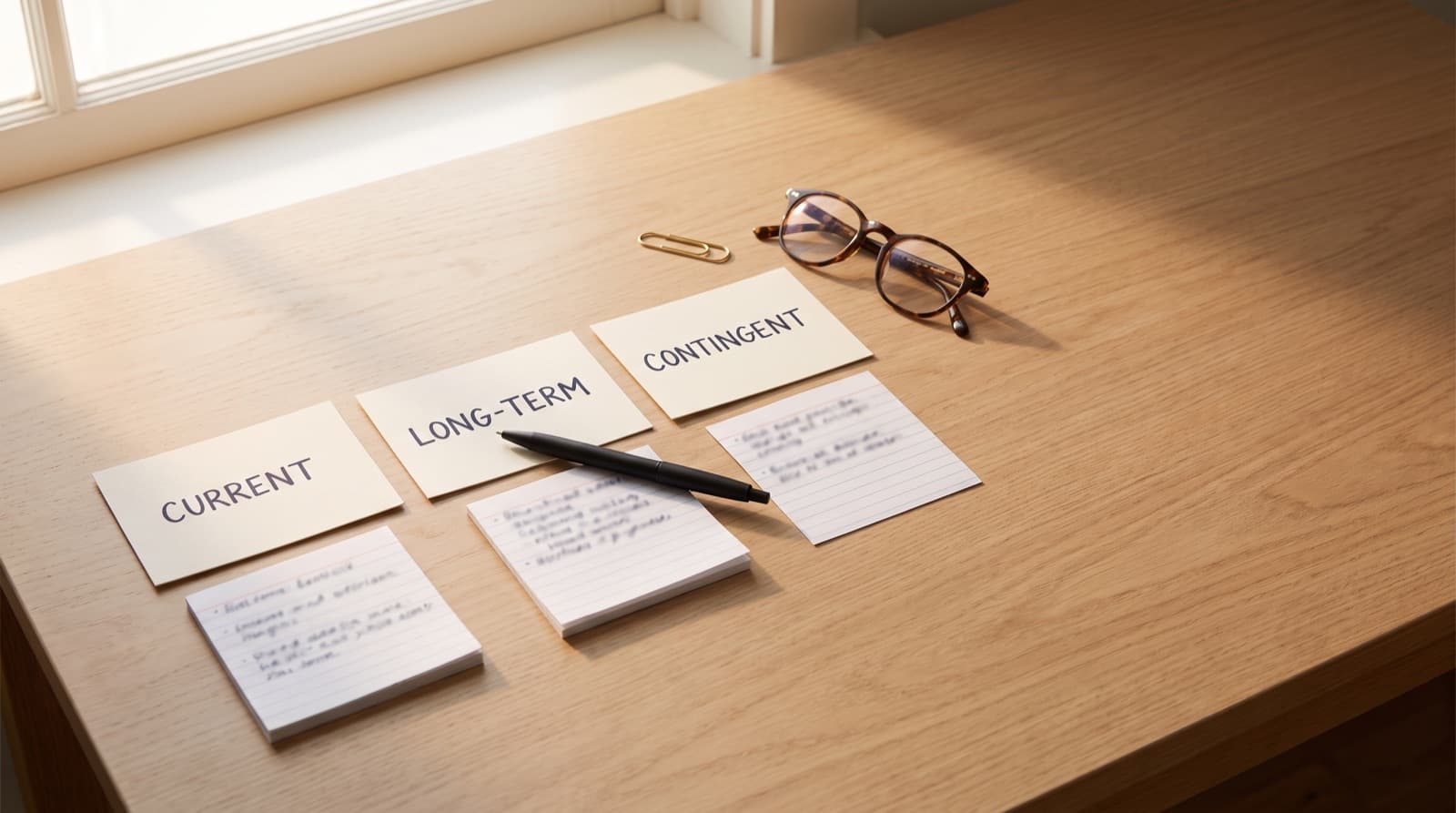

The 7 types of liabilities — current, long-term, contingent, secured, unsecured, joint, and tax — and exactly where each one lands on a personal financial statement.

Five net worth statement examples with real numbers: W-2 earner, business owner, real estate investor, retiree, and SBA borrower, plus what a lender reads first.

A complete list of assets and liabilities with 50+ examples, organized the way lenders read them on a personal financial statement.

Commercial real estate loan qualifications come down to DSCR, LTV, debt yield, and your personal balance sheet. Here is exactly what lenders check.

How an SBA 504 loan finances owner-occupied commercial real estate: the 50-40-10 two-loan stack, the fixed-rate CDC debenture, 25-year terms, and why it beats a 7(a).

SBA 504 loan requirements for 2026: the 50-40-10 structure, the 51% occupancy rule, the job-creation test that changed, and the Form 413 every owner files.

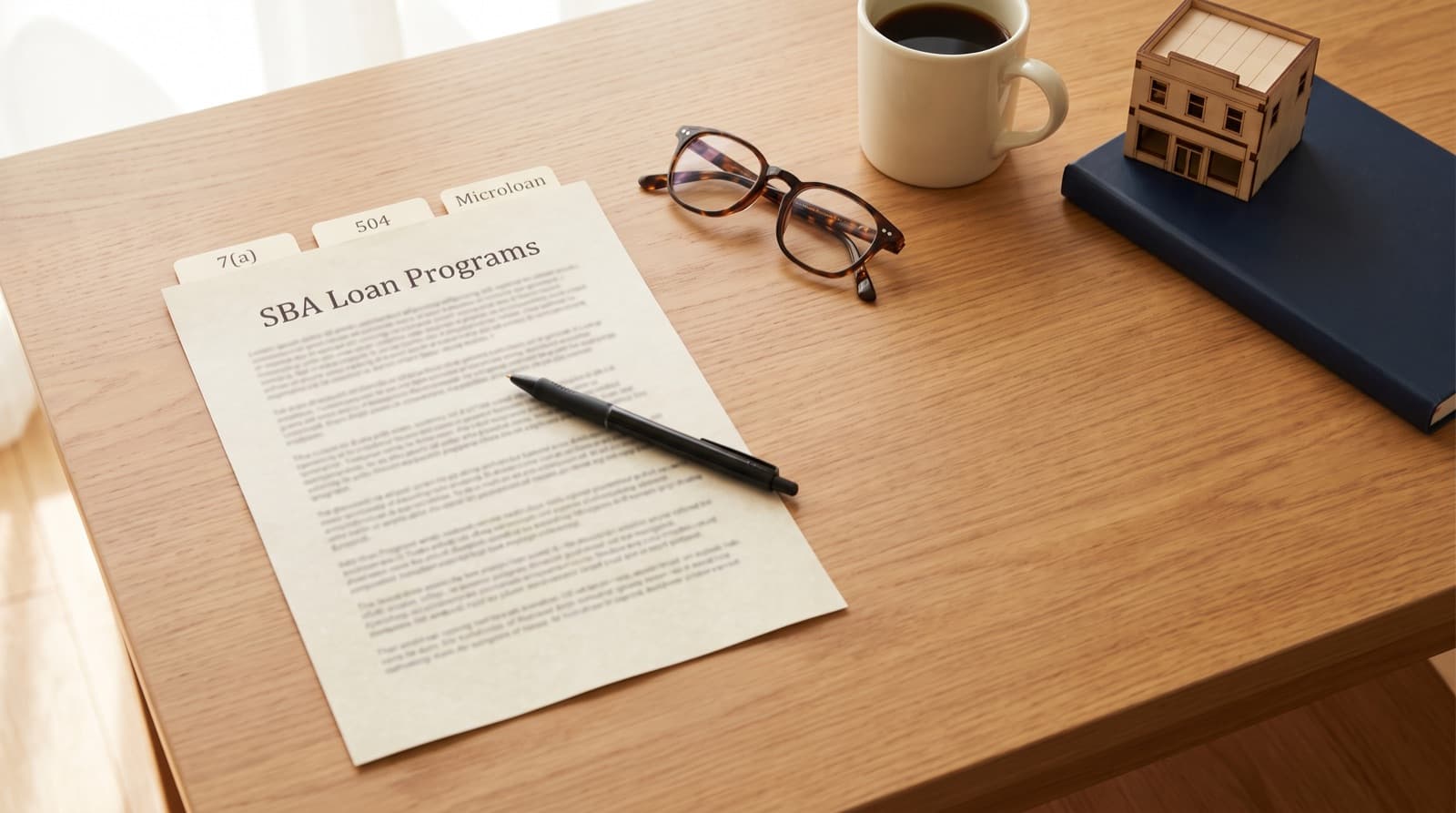

An SBA loan is a small-business loan the government partly guarantees. Here are the 7(a), 504, and microloan programs, 2026 rates, and the documents you prepare.

SBA 7(a) and 504 loans can't finance a passive rental property; the owner-occupancy rule blocks it. Here's what qualifies and the DSCR alternative.

DSCR loan pros and cons for investors: qualify on rent instead of income and skip the 10-property cap, but pay 20–25% down, a higher rate, and a prepay penalty.

A DSCR loan down payment usually runs 20–25% (75–80% LTV), but your DSCR ratio, credit score, and property type move it. Here's the 2026 breakdown.

A DSCR loan for investment property qualifies on the rental's cash flow instead of your income — so you can scale past the conventional 10-property wall. Here's how.

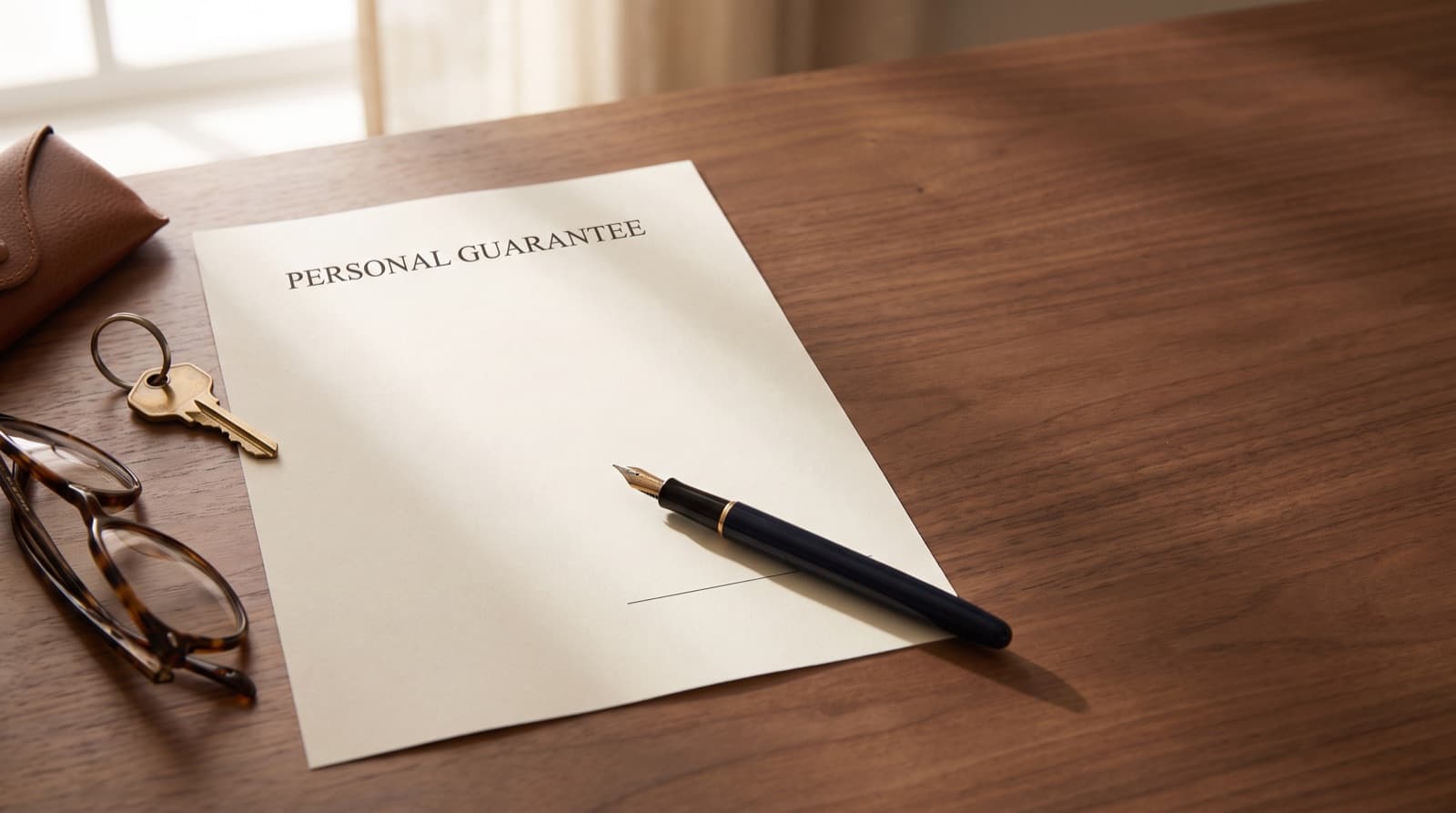

A personal guarantee makes you repay a business loan from your own assets if the company defaults. Here is who signs, what it binds, and how to limit it.

The New York Statement of Net Worth is the sworn financial disclosure every divorcing spouse files under DRL 236. Here is how to complete it right.

SBA loan down payment rules in 2026: the 10% equity injection on 7(a) startups and buyouts, the 504 50/40/10 split, and which funds actually count.

Commercial real estate loan terms cover term length, amortization, LTV, DSCR, recourse, and rate. Here is what each one means before you sign.

Excel's built-in gallery has budget and net worth templates, but no lender-style personal financial statement. Here is what to download instead.

A net worth statement lists what you own minus what you owe on one dated page. Here's what goes on it, who asks for it, and how it differs from a PFS.

SBA 7(a) loan requirements changed in 2026: SOP 50 10 8 eligibility, equity injection, credit, collateral, citizenship, and the Form 413 every owner files.

SBA 7(a) vs. 504 loan, compared for 2026: structure, rates, down payment, fees, and eligible uses, plus which program fits owner-occupied real estate.

How to calculate DSCR step by step: build NOI, total your annual debt service, divide, and reverse the formula to find the maximum loan your property supports.

A DSCR loan qualifies you on your rental property's cash flow, not your personal income or tax returns. Here is how the ratio works and what lenders want.

A personal financial statement helps first-time homebuyers size up net worth, DTI, and cash to close before a lender ever opens the application.

Net worth for an SBA loan is total assets minus total liabilities on Form 413. Here is how to calculate it, value each line, and what lenders do with it.

Personal financial statement signature requirements for SBA Form 413: who signs, when a spouse signs, the 120-day dating rule, and e-sign vs. wet ink.

SBA 504 personal guarantee requirements explained: who must sign an unlimited guaranty, how the bank and CDC differ, and when a guarantee can be limited.

How the self-employed build a personal financial statement, and how lenders rebuild Schedule C net profit into the qualifying income that backs the loan.

The common SBA Form 413 mistakes that get a personal financial statement returned in underwriting, and how to fix each one before you submit.

A net worth statement template lists what you own, values it at today's market price, and subtracts your debts. Here is how to build yours in 20 minutes.

A personal financial statement Excel template is free and works for one filing. See where it breaks on repeat lender requests, and when PFS software wins.

Who must submit a personal financial statement (SBA Form 413) for a 7(a) loan, the 20% guaranty trigger, spousal rules, and what underwriters check.

A personal financial statement is a point-in-time snapshot. Refresh it within 120 days for an SBA 7(a)/504 loan, yearly otherwise, and after a major change.

A personal financial statement for divorce inventories every asset and debt before you sign the court's sworn disclosure. Here is how to build one right.

A DSCR loan qualifies the property; a personal-income mortgage qualifies you. Here's what each one asks for, what it costs, and when to choose which.

A personal financial statement and a balance sheet both subtract what you owe from what you own. Here's what each shows and which a lender asks for when.

A personal financial statement is a dated snapshot of your assets, liabilities, and net worth. Here's what goes on one, who needs it, and how lenders read it.

On the current SBA Form 413, contingent liabilities sit beside Section 1, not in Section 5. Here is what counts on each of the four lines.

DSCR loan requirements in 2026: the minimum ratio, FICO, down payment, and reserves most lenders set, plus the borderline cases that still get funded.

What every business-loan lender, SBA or conventional, actually looks at on your personal financial statement, plus the thresholds underwriters quietly use.

SBA Form 413 is the personal financial statement every 20%+ owner of an SBA 7(a) or 504 borrower submits. Here is how to fill out each section.

A personal financial statement template captures your assets, liabilities, and net worth on a short balance-sheet form. Here is what each section needs.

A real example of a completed SBA Form 413 for a hypothetical 7(a) applicant, with every line annotated — what underwriters see and why it matters.