SBA Lending

How to Fill Out SBA Form 413: A Section-by-Section Guide

SBA Form 413 is the personal financial statement every 20%+ owner of an SBA 7(a) or 504 borrower submits. Here is how to fill out each section.

22 min read

SBA Form 413 is the Personal Financial Statement required for SBA 7(a), 504, microloan, and disaster loan applications. This guide walks the form line by line, covers who must complete it, and lists the mistakes that delay or kill loan approvals.

Updated for 2026 · Published 2023 · Last reviewed May 2026

SBA Form 413, officially titled "Personal Financial Statement," is the standardized financial disclosure form required by the Small Business Administration (SBA) for anyone applying for an SBA-backed loan. This includes SBA 7(a) loans, SBA 504 loans, SBA microloans, and SBA disaster loans.

The form requires you to provide a complete snapshot of your personal financial situation, including all assets, liabilities, income sources, and contingent obligations. Lenders use this information to assess your personal financial strength, creditworthiness, and ability to repay the loan if your business cannot.

Why is it required? The SBA guarantees a portion of the loan, which reduces risk for lenders. However, they still need to verify that you, as the business owner, have the personal financial capacity to support the business if needed. Your personal financial statement serves as collateral and demonstrates your commitment to the business.

⚠️ Criminal Penalties Warning

The SBA Form 413 includes a statement warning that knowingly making a false statement to obtain a loan from the SBA is a violation of Federal law under 18 U.S.C. 1001 and could result in criminal prosecution, fines up to $250,000, and imprisonment up to 5 years. Accuracy and honesty are not optional—they're legally required.

The SBA requires a Personal Financial Statement (Form 413) from:

💡 Pro Tip: Even if you're not required to submit a personal financial statement, having one prepared can speed up your loan application and demonstrate financial preparedness to lenders.

Form 413 is required for every SBA-backed loan that involves a personal guarantee. The threshold and timing vary slightly by program:

| SBA Loan Program | Form 413 Required? | Who Must Submit |

|---|---|---|

| SBA 7(a) — General business loans up to $5M | Yes | All 20%+ owners, general partners, managing LLC members, and any personal guarantor |

| SBA 504 — Real estate & equipment financing | Yes | Same as 7(a). CDC and lender both review. |

| SBA Microloan — Up to $50,000 | Usually yes | Owner(s) of the borrowing business. Some intermediaries use a simplified form. |

| SBA Disaster Loan (EIDL) | Yes, typically alongside disaster-specific forms | All principals with 20%+ ownership |

| SBA Express — Expedited 7(a) variant | Yes | Same as 7(a) |

Refer to: The official Personal Financial Statement is published by the U.S. Small Business Administration as Form 413 (OMB Approval No. 3245-0188). Lenders participating in SBA programs are required to collect it under SBA SOP 50 10.

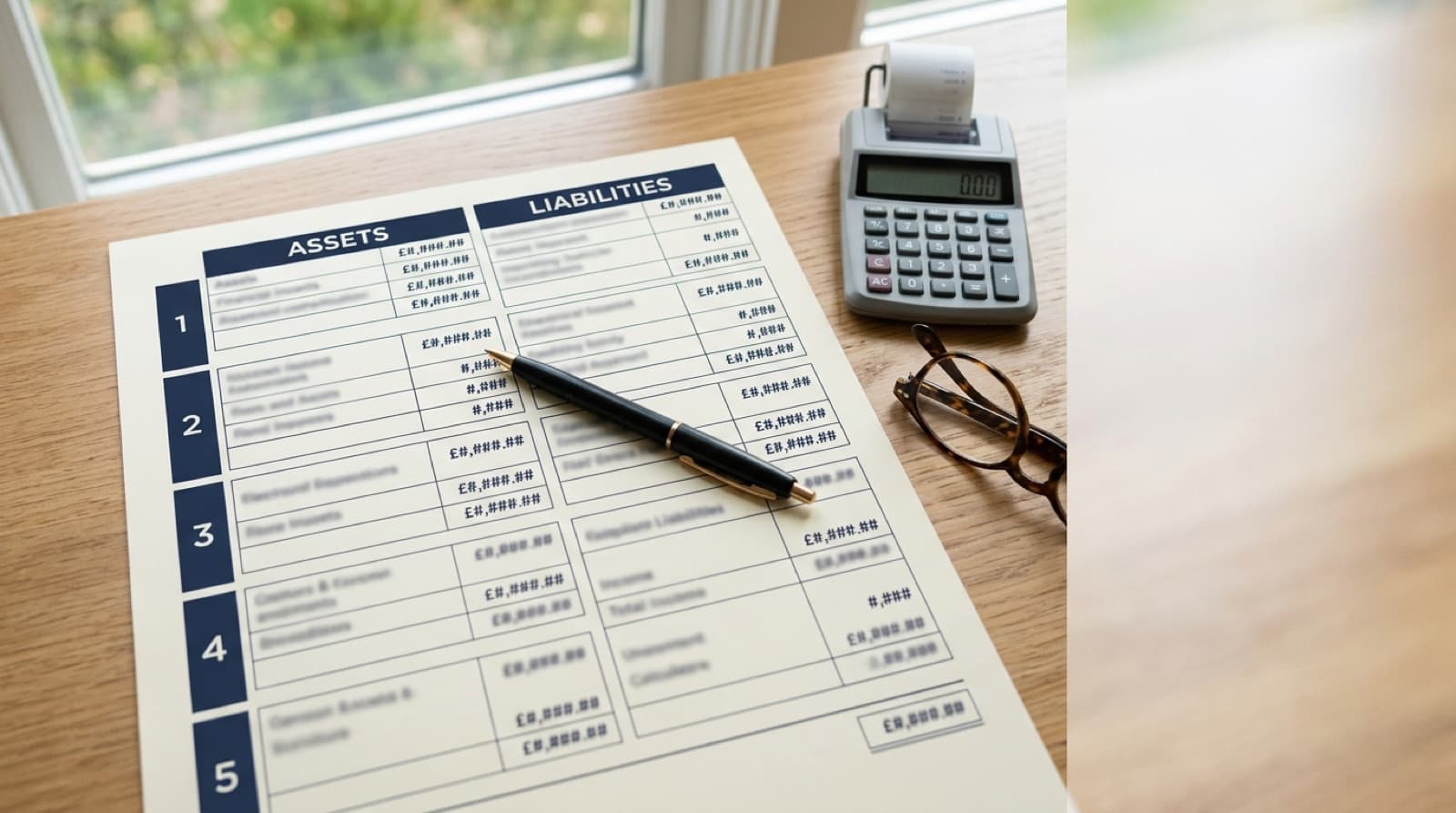

The SBA Form 413 is divided into several sections. Here's a detailed breakdown of what you'll need to provide:

This is the core of the form. You'll list all assets with their current market value and all liabilities with their current balance. The difference between total assets and total liabilities is your net worth.

Formula: Net Worth = Total Assets - Total Liabilities

You must provide a detailed schedule of all real estate you own, including:

For each stock or bond holding, provide:

The SBA Form 413 has limited space on the main form. If you have more items than can fit, overflow items must be placed on separate schedules.

| Section | Main Form Capacity | Overflow Schedule |

|---|---|---|

| Real Estate Properties | 3 properties | Schedule C |

| Stocks, Bonds & Securities | 4 items | Schedule B |

| Notes Payable | 5 items | Schedule A |

When you use StatementsReady, our system automatically detects when you exceed these limits.

A line-by-line walkthrough. Pull statements from each financial account before you start — the form requires balances as of the same statement date, not "approximately current."

Use your full legal name as it appears on government ID. Residence address is your physical home address, not a P.O. box. Business name is the legal entity name of the borrower — not a DBA. Enter the statement date (the "as of" date for every balance you'll list).

Sum of all checking, savings, money market, and CD balances as of the statement date. Use the statement closing balance, not the current online balance, unless they match exactly. Round to the nearest dollar.

List the full current balance of 401(k), traditional IRA, Roth IRA, SEP-IRA, SIMPLE IRA, 403(b), and pensions with a defined balance. Some lenders apply a discount for taxes and early-withdrawal penalties; ask before submitting. List the gross balance unless instructed otherwise.

Money owed to youpersonally. Include personal loans you've made, seller-financed notes you hold, and judgments in your favor that are collectible. Don't include amounts owed to your business — those belong on the business's balance sheet.

Cash surrender value, not the face value (death benefit). For whole life and universal life policies, request the current surrender value from your insurer. Term life has no cash value — list zero.

Current market value of brokerage accounts, individual stocks, bonds, ETFs, and mutual funds. Use the closing price on the statement date. If you hold more than four positions, complete Schedule B and reference it.

Current market value, not purchase price or Zillow Zestimate. For each property, document address, type, date acquired, original cost, mortgage balance, monthly payment, and rental income. Be conservative — lenders will appraise.

Current fair market value, not book value or purchase price. Use Kelley Blue Book or NADA for a defensible number. Include cars, trucks, motorcycles. Subtract any auto loan balance on the liabilities side, not here.

Personal loans, lines of credit, and bank notes in your name. For each, list creditor name, original balance, current balance, monthly payment, due date, and collateral. Five or more items overflow to Schedule A.

Installment accounts include auto loans, student loans, and consumer financing — separate monthly payments for autos vs. other. Mortgages: list current balance for each property (must match real estate schedule). Taxes: only unpaid balances, not estimated future taxes.

Loans you've co-signed or personally guaranteed for another business, individual, or property. Pending lawsuits where you're named. Disputed federal income tax liabilities. Omitting these is a leading cause of loan denial — lenders cross-check with credit reports and they will find them. See our full breakdown of SBA Form 413 contingent liabilities for worked examples.

Annual amounts. Salary is gross W-2 wages. Net investment income is dividends + interest + capital gains net of investment expenses. Real estate income is gross rents minus expenses. Other income covers business distributions, royalties, alimony received, and trust distributions.

Both signatures (yours and spouse's, where required by state law or lender) and the date must appear. In community property states, spouse signature is typically required even on separate property. An unsigned form is the #1 cause of same-day rejection.

StatementsReady pulls balances from 12,000+ banks via Plaid, applies SBA Form 413 categorization automatically, generates Schedules A, B, and C when overflow is needed, and exports an SBA-compliant PDF — typically in under 10 minutes total.

Auto-Fill SBA Form 413 FreeThese errors can delay your loan application or even result in denial. Avoid them at all costs:

Lenders expect current, accurate balances as of the statement date. Using numbers from 6 months ago or "guessing" at account balances will raise red flags. Log into each account and get exact balances, or use StatementsReady to sync balances automatically via Plaid.

If you've co-signed a loan, guaranteed a debt, or are liable for someone else's obligation, it must be disclosed—even if you're not currently making payments. Failing to disclose contingent liabilities is a common reason for loan denial.

Use realistic, conservative market values for real estate. Don't use Zillow "Zestimates" or wishful thinking. Lenders will order appraisals, and inflated values will damage your credibility and could be considered fraud.

For life insurance, you must list the cash surrender value (what you'd get if you cashed it in today), NOT the face value (death benefit). These are very different numbers.

Both you and your spouse (if married) must sign and date the form. An unsigned or partially signed form will be rejected immediately. Some states require spouse signatures even for separate property.

Don't skip the $500 credit card balance or the $2,000 savings account because they seem insignificant. List everything. Lenders will pull your credit report and bank statements— omissions look like you're hiding something.

If you get married, divorced, buy a house, or have any major financial change during the loan process, you must update your personal financial statement. Using an outdated statement can invalidate your application.

Some lenders want you to discount retirement account values by estimated taxes and early withdrawal penalties. Ask your lender how they want 401(k) and IRA accounts valued before submitting.

For assets like cars and real estate, use current market value (what you could sell it for today), not what you paid for it (book value) or what you think it's worth.

While technically allowed, handwritten forms are harder to read, more prone to errors, and look unprofessional. Use a typed, digital version for a polished, professional presentation.

Manual Method

Logging into 10+ accounts, copying numbers to Excel, formatting, calculating, double-checking math, and praying you didn't make a mistake.

Using Excel Templates

Faster than starting from scratch, but still requires manual data entry, formula checks, and formatting fixes.

Using StatementsReady

Connect your accounts, let AI categorize everything, review, sign, and export. Done. Accurate. Professional.

We've automated the painful parts and added intelligence to ensure accuracy and compliance.

Connect 12,000+ banks and investment accounts via Plaid. Balances sync automatically— always current, always accurate. No more logging into a dozen accounts.

Our AI assistant automatically categorizes assets and liabilities correctly, suggests proper valuations, and flags potential errors before you submit.

Generate a perfectly formatted, professional PDF that matches SBA Form 413 requirements exactly. No more fighting with Excel formatting or worrying about compliance.

Sign electronically and send to your spouse for signature. No printing, scanning, or mailing. Fully legally binding and accepted by all SBA lenders.

Manage multiple properties with detailed schedules. Track mortgages, rental income, and property values all in one place. Perfect for real estate investors.

Net worth, total assets, total liabilities—all calculated automatically with zero math errors. We even validate your numbers against common mistakes.

Free trial • No credit card required • 8-minute setup

Yes, if you have an ongoing relationship with an SBA lender (like a line of credit or annual review requirement), you'll need to submit an updated personal financial statement annually. StatementsReady makes this easy with one-click annual rollover—your data carries forward, and you just update the balances.

Some lenders accept alternative personal financial statement formats, but SBA Form 413 is the standard and most widely accepted. If you use an alternative format, make sure it includes all the same information required by Form 413. StatementsReady generates multiple professional formats that meet or exceed SBA requirements.

A negative net worth (liabilities exceed assets) doesn't automatically disqualify you from an SBA loan, but it makes approval more difficult. Lenders will look at your income, business cash flow, and other factors. Be honest—lying about your financial situation is fraud and will result in immediate denial and potential legal consequences.

List the actual date you purchased each property, regardless of how long ago it was. This helps lenders assess appreciation and your investment track record. If you inherited property, use the date you received it.

This depends on your state's community property laws and lender requirements. In community property states (AZ, CA, ID, LA, NV, NM, TX, WA, WI), you typically must include all marital assets and liabilities. In other states, you may be able to file separately. Ask your lender for guidance, and have your spouse complete their own Form 413 if required.

Honest mistakes can be corrected by submitting an amended statement. However, intentional misrepresentations or material omissions can result in loan denial, loan recall, and criminal prosecution. Always double-check your numbers and be conservative with valuations.

For active 7(a) or 504 loan applications, the current Form 413 must be dated within 120 days of submission (90 days for Disaster loans). For annual reviews, update it once per year. For your own financial planning, updating quarterly gives you a clear picture of your wealth trajectory. StatementsReady makes updates instant with automatic bank syncing.

Download the official blank form directly from the SBA website. Or skip the manual work and let StatementsReady fill it out for you automatically.

Join thousands of real estate investors and business owners who've ditched spreadsheets for automated, accurate, and professional personal financial statements.

Start Your Free Trial Today✓ No credit card required ✓ 8-minute setup ✓ Cancel anytime

SBA Form 413 is the personal financial statement every 20%+ owner of an SBA 7(a) or 504 borrower submits. Here is how to fill out each section.

A real example of a completed SBA Form 413 for a hypothetical 7(a) applicant, with every line annotated — what underwriters see and why it matters.

On the current SBA Form 413, contingent liabilities sit beside Section 1, not in Section 5. Here is what counts on each of the four lines.